TL;DR

- Your FIRE number doesn't change much by age. At $60k/year spending, you need ~$1.5M whether you retire at 35 or 50.

- What changes: how much you need to save monthly to get there, and how long your money needs to last.

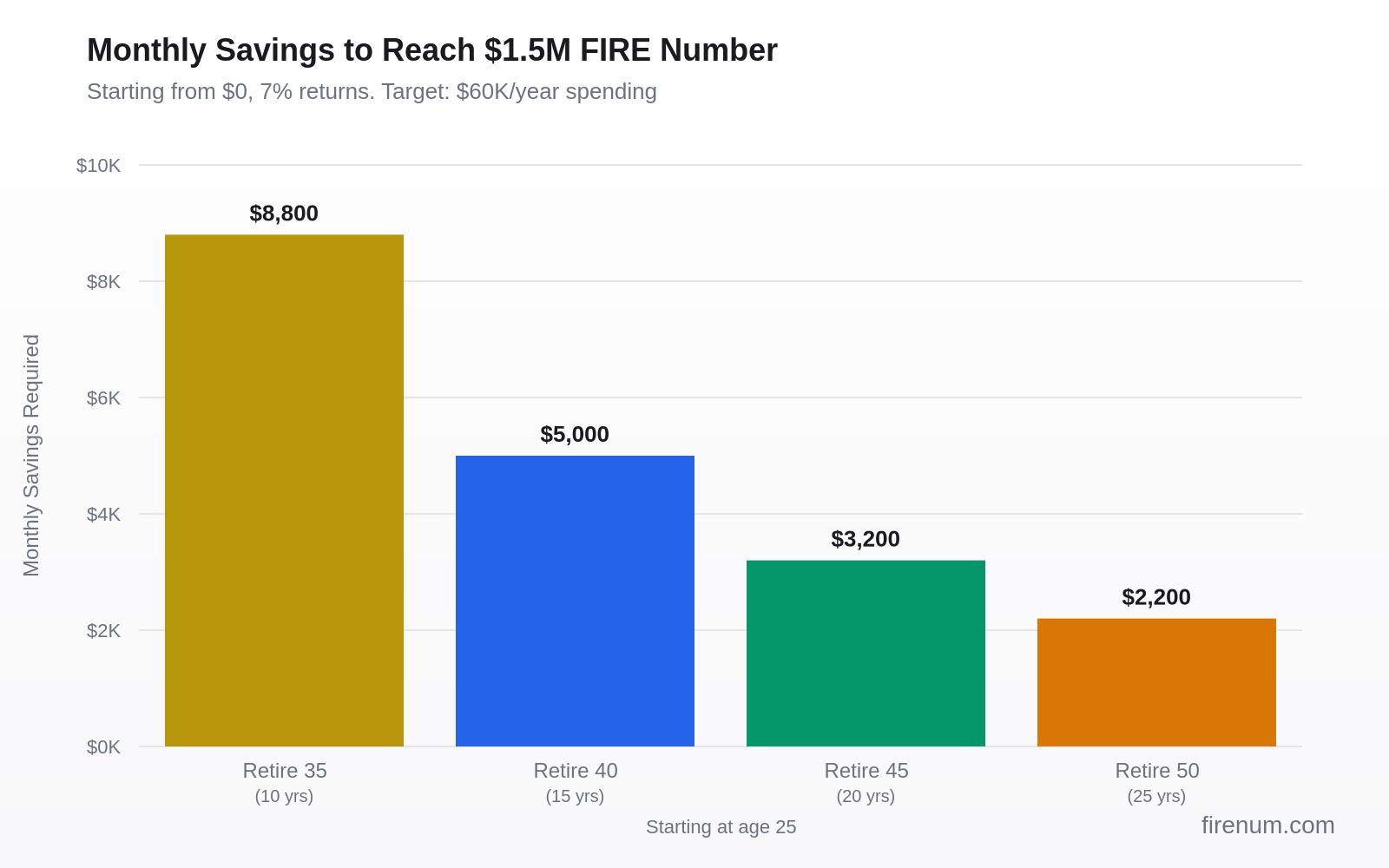

- Retire at 35 from scratch? You need ~$8,800/month saved for 10 years.

- Retire at 50 from scratch? You need ~$2,200/month saved for 25 years.

- The hard parts aren't the math. Healthcare, account access before 59.5, and 50+ years of inflation are the real challenges.

The Simple Math

Your FIRE number is straightforward: annual expenses x 25. This is based on the 4% rule — withdraw 4% of your portfolio each year, and it should last 30+ years.

William Bengen, who first published the 4% rule in 1994, has noted: "For very long time horizons, I would recommend a withdrawal rate closer to 3.0-3.5%. The original research wasn't designed for 50-year retirements." This is especially relevant when retiring at 35 or 40.

Spend $60,000/year? You need $1,500,000. Spend $40,000/year? You need $1,000,000.

Notice what's not in that formula: your age. The FIRE number is the same whether you're 25 or 55. What changes with age is everything else — how aggressively you need to save, how long your money needs to last, and what risks you face along the way.

Know your spending number? Plug it into our FIRE Number Calculator to see your exact target in 2 seconds.

FIRE Number by Spending Level

Before we talk about age, let's anchor on the target. Here's what different spending levels require:

| Annual Spending | FIRE Number (25x) | Conservative (28x) | Monthly Safe Withdrawal |

|---|---|---|---|

| $30,000 | $750,000 | $840,000 | $2,500 |

| $40,000 | $1,000,000 | $1,120,000 | $3,333 |

| $50,000 | $1,250,000 | $1,400,000 | $4,167 |

| $60,000 | $1,500,000 | $1,680,000 | $5,000 |

| $80,000 | $2,000,000 | $2,240,000 | $6,667 |

| $100,000 | $2,500,000 | $2,800,000 | $8,333 |

The "Conservative (28x)" column uses a 3.5% withdrawal rate instead of 4%, which adds a safety margin for retirements longer than 30 years. If you're retiring before 45, the conservative number is worth considering.

For a deeper look at why the 4% rule holds up (and when it doesn't), see our recent analysis of Morningstar's 2026 data.

How Much You Need to Save Monthly

This is the real question. The FIRE number is a destination. The monthly savings rate is how fast you're driving.

The table below assumes you're starting from $0, earning a 7% nominal return (roughly the long-term average for a stock-heavy portfolio), and targeting a $1,500,000 FIRE number ($60,000/year spending).

| Current Age | Retire at 35 | Retire at 40 | Retire at 45 | Retire at 50 |

|---|---|---|---|---|

| Age 25 | $8,800/mo (10 yrs) | $5,000/mo (15 yrs) | $3,200/mo (20 yrs) | $2,200/mo (25 yrs) |

| Age 30 | $24,600/mo (5 yrs) | $8,800/mo (10 yrs) | $5,000/mo (15 yrs) | $3,200/mo (20 yrs) |

| Age 35 | -- | $24,600/mo (5 yrs) | $8,800/mo (10 yrs) | $5,000/mo (15 yrs) |

Some of these numbers look brutal. $8,800/month starting from zero requires a high income and aggressive savings rate. That's why most people who retire at 35 either (a) started early and had time on their side, (b) had very high incomes in tech/finance/medicine, or (c) had a windfall event like stock options or inheritance.

The more realistic scenario: you start at 25, already have some savings, and the required monthly contribution is lower. Even $100,000 saved by age 25 drops the "retire at 40" monthly requirement from $5,000 to roughly $3,800.

Want your exact number? Our How Much to Save Calculator factors in your current savings, expected return, and target to give you the precise monthly amount.

The Age-Specific Challenges

Retire at 35: The Long Road

Years in retirement: 50-60+

This is the hardest target. Not because the math is impossible, but because the non-financial challenges compound:

- 50+ year horizon: Your money needs to survive multiple market cycles, recessions, and potentially extended periods of high inflation. A 3.0-3.5% withdrawal rate is prudent.

- Healthcare gap: 30 years without employer healthcare before Medicare at 65. In the US, budget $12,000-$30,000/year for family coverage, depending on subsidies.

- The 59.5 rule: Most retirement accounts (401k, Traditional IRA) penalize withdrawals before age 59.5. You need taxable accounts, Roth conversion ladders, or Rule 72(t) distributions to bridge the gap.

- The boring middle: You've likely only been working 10-13 years. Saving aggressively enough to retire this fast usually means an income north of $150,000 or an extremely frugal lifestyle.

Who actually pulls this off? Usually high-income tech or finance workers, dual-income couples with aggressive savings rates, or people who combined moderate income with extreme frugality (the classic "leanFIRE" path).

Retire at 40: Ambitious but Achievable

Years in retirement: 45-50+

This is the most common target in FIRE communities. You have 15-18 working years if you start in your early 20s, which is enough time for compound growth to do meaningful work.

- Still a long horizon: 45+ years means you should lean toward the conservative 28x multiplier. But flexible spending makes 25x workable.

- Career capital: By 40, you likely have significant skills and earning potential. Going back to work if needed is a realistic safety net.

- The math is friendlier: Starting at 25 with $5,000/month invested is aggressive but achievable on a $100,000+ household income with a 60%+ savings rate.

- Healthcare still matters: 25 years until Medicare. Budget for it explicitly.

Consider Coast FIRE as a stepping stone: hit your Coast number by 35, then reduce work intensity while your investments grow.

Retire at 45: The Sweet Spot

Years in retirement: 40-45+

For many people, this is where the math gets comfortable. You have 20-23 working years, compound interest has had real time to build, and the monthly savings requirement is manageable on a middle-class income.

- Only 14.5 years to bridge until the 59.5 penalty-free withdrawal age. A Roth conversion ladder started at 40 covers this gap nicely.

- Career fatigue peaks: Research consistently shows job satisfaction drops sharply in the 40-50 age range. Having the option to stop is powerful even if you choose to continue.

- Social Security is closer: Only 17-22 years until benefits begin, which reduces your long-term withdrawal needs.

- Kids may be leaving: If you had children in your late 20s/early 30s, they're approaching independence. Your expenses may drop naturally.

Retire at 50: The Forgiving Path

Years in retirement: 35-40+

This is close to traditional early retirement, and the math is the most forgiving:

- 9.5 years to 59.5: Easily bridged with taxable accounts, Roth contributions (not conversions), or Rule of 55 if you leave your employer after age 55.

- 15 years to Medicare: Still a healthcare gap, but a manageable one. Many employers offer retiree healthcare or COBRA bridges.

- Social Security at 62: Only 12 years away. Even reduced benefits at 62 significantly decrease your withdrawal needs.

- Standard 4% rule works: A 35-40 year horizon is close enough to the original 30-year research that 25x is a solid target without needing the conservative multiplier.

- Lower monthly savings: Starting at 25, you need $2,200/month — achievable on a $70,000+ income with a solid savings rate.

Find your date. Our When Can I Retire Calculator tells you the exact year based on your current savings, income, and spending.

What Most Guides Get Wrong

Every "how much to retire early" article gives you the FIRE number and stops. But the FIRE number is the easy part. Multiply your expenses by 25. Done. The hard parts are everything that comes after:

As Morningstar's Christine Benz has emphasized: "The biggest risk for early retirees isn't running out of money. It's the non-financial challenges — healthcare, identity, and the sheer length of time your plan needs to survive."

Healthcare Before 65 (US-Specific)

This is the single biggest non-investment expense for early retirees in the US. ACA marketplace plans for a family of 4 can run $18,000-$30,000/year without subsidies. The good news: if your retirement income is low enough (which it often is when you're living off capital gains and Roth conversions), you may qualify for substantial ACA subsidies.

The Social Security Administration provides detailed calculators for estimating your future benefits, which is useful for planning the second half of an early retirement.

Build healthcare into your annual expense estimate before calculating your FIRE number. If healthcare adds $15,000/year to your expenses, your FIRE number goes up by $375,000.

Accessing Retirement Accounts Before 59.5

You've maxed your 401k for 15 years. Great — but that money is locked until 59.5 (with penalties for early withdrawal). Three main workarounds:

- Roth Conversion Ladder: Convert Traditional IRA money to Roth each year. After a 5-year seasoning period, you can withdraw the converted amount penalty-free. Start conversions 5 years before you need the money.

- Rule of 55: If you leave your employer during or after the year you turn 55, you can access that employer's 401k penalty-free. Only applies to the 401k from your last employer.

- 72(t) / SEPP: Substantially Equal Periodic Payments from an IRA. Complex rules, but allows penalty-free access at any age. The payments must continue for 5 years or until 59.5, whichever is later.

The practical advice: keep 5-7 years of expenses in taxable accounts and/or Roth contributions (not earnings) that you can access without restrictions.

Inflation Over 50+ Years

At 3% inflation, $60,000/year in today's dollars becomes roughly $262,000/year in 50 years. The 4% rule accounts for inflation (withdrawals increase each year), but the psychological impact of watching your nominal expenses quadruple is real.

This is another argument for flexible spending strategies and maintaining some earning capacity. See our analysis of the 4% rule for more on how flexibility changes the math.

The "Boring Middle"

The hardest phase of FIRE isn't the beginning (when motivation is high) or the end (when the finish line is visible). It's the middle — years 4-12 of saving — when compound growth hasn't kicked in yet, the novelty has worn off, and the goal still feels impossibly far away.

This is where most people quit. Not because the math stopped working, but because the psychology is brutal. The best antidote is tracking your progress and seeing the numbers move. Even small gains compound into significant portfolio growth over time.

Frequently Asked Questions

The original 4% rule was designed for 30-year retirements. For 50+ year horizons, most researchers recommend a 3.0-3.5% withdrawal rate. However, flexible spending strategies and the ability to earn supplemental income give early retirees safety valves that traditional retirees don't have. Using 4% (25x expenses) as your target is reasonable if you're willing to adjust spending when markets are bad.

In the US, healthcare before Medicare eligibility at 65 is a major consideration. ACA marketplace plans for a family can cost $1,500-$2,500/month without subsidies. If your retirement income is low enough (under ~$80,000 for a family of 4), you may qualify for significant ACA subsidies. Many early retirees plan for this by including healthcare as a separate expense line item in their FIRE calculations.

Generally, no — unless you plan to sell it and use the proceeds to fund retirement. Your FIRE number should represent investable assets that generate income. A paid-off home reduces your expenses (no rent or mortgage), which lowers your FIRE number. But the home equity itself isn't producing cash flow for withdrawals.

A pension reduces the amount you need from your portfolio. If your pension covers $20,000/year of expenses and you spend $60,000/year total, you only need to cover $40,000/year from withdrawals. That means your FIRE number drops from $1,500,000 to $1,000,000. Calculate: (total expenses minus pension income) times 25.

If you retire early, Social Security kicks in at 62 (reduced benefit) or 67 (full benefit). For early retirees, plan to fully fund your spending from age of retirement to 62-67 without Social Security. After that, your portfolio withdrawal needs drop. Many FIRE planners treat Social Security as a bonus rather than a pillar of their plan — if it's there, great; if benefits are reduced, you're still fine.

The US stock market has returned approximately 10% nominally (7% after inflation) over the long term. Most FIRE planners use 7% nominal (which is conservative and roughly accounts for a stock-heavy portfolio) or 5% real (inflation-adjusted). Using 7% nominal is a reasonable middle ground for accumulation-phase projections. Be more conservative (5-6%) if you want a larger safety margin.

Ready to calculate your exact number?