TL;DR

- You don't need a $200K tech salary. 20% of Reddit $1M+ milestone posters never earned over $100K

- Savings rate beats income. 50% savings rate on $60K beats 10% on $150K every single time

- Time is the equalizer. Starting at 22 instead of 30 can mean $500K+ more by 45

- It takes longer, but it works. Normal-salary FIRE is a 15\u201325 year game, not a 5\u201310 year sprint

The Myth That FIRE Requires a Big Salary

Spend five minutes in any FIRE subreddit and you'll notice a pattern. Software engineers making $300,000. Dual-income couples pulling $400,000. Posts that casually mention "maxing out both 401ks and backdoor Roths" like everyone has $50,000 in annual retirement contributions lying around.

"I feel like I don't belong here. Everyone seems to be a software engineer making $400K. I'm a teacher pulling $52K and wonder if FIRE is even possible for me." -- r/financialindependence

The perception has shifted. FIRE went from a frugality movement to what feels like a high-income-earners club. But the data tells a different story.

The Numbers Don't Lie

We analyzed real FIRE milestone posts on Reddit and found something the online discourse doesn't reflect: 20% of $1M+ milestone posters never earned over $100,000.

The most striking example was a 39-year-old in NorCal with $2.4M in net worth who never earned more than $80,000:

"I've never made more than $80k, which is below average income in my NorCal city. Reaching $1M in my IRA accounts was the final silly goalpost I set for myself." -- 39yo with $2.4M net worth

Or the 46-year-old woman who FIRE'd with $1.5M from a career in insurance management while her husband worked at a hardware store. Four kids. No tech salaries. No inheritance.

"We didn't have tech salaries or come from wealthy families, and we had four kids to raise." -- 46F who FIRE'd at 45 with $1.5M

Another poster hit $1M at age 40 while earning $73,000 -- the same job for 15 years. No job-hopping. No side hustles. Just consistent investing over a long period.

Where do you stand? See the full dataset in our Reddit Milestone Analysis.

The Real Strategies: What Under-$100K Earners Do Differently

Savings Rate Over Income

This is the single most important insight in FIRE, and it matters even more at lower incomes. A 50% savings rate on $60,000 means $30,000 saved per year. A 10% savings rate on $150,000 means $15,000 saved per year.

The person earning $60,000 is saving twice as much and proving they can live on half as much. That's a devastating combination: they need less money to retire AND they're accumulating it faster relative to their goal.

Time in Market

This is where normal-salary earners have a secret weapon: time. Starting at 22 instead of 30 doesn't just add 8 years of contributions. It adds 8 years of compound growth on every dollar you invest.

Here's the math. Invest $500/month at 7% average returns:

- Start at 22, stop at 45: ~$400,000 (23 years of contributions)

- Start at 30, stop at 45: ~$190,000 (15 years of contributions)

- Difference: $210,000 -- mostly from compound growth, not extra contributions

The NorCal poster who hit $2.4M on under $80K? Started investing at 22. That 17 extra years of growth did the heavy lifting.

Geographic Arbitrage

A $50,000 salary in San Francisco is a struggle. The same $50,000 in Omaha, Raleigh, or Boise can fund a comfortable life with a 40%+ savings rate. Many normal-salary FIRE achievers deliberately choose lower cost-of-living areas -- or work remotely from them.

Housing Hacks

Housing is the biggest expense for most people, and it's where normal-salary FIRE people get creative:

- Roommates for a decade. The $2.4M NorCal poster lived with roommates through most of his 20s and 30s

- House hacking. Buy a duplex, live in one unit, rent the other. Your mortgage is partially or fully covered

- Dramatic downsizing. The family of six downsized from 2,500 to 1,000 square feet and freed up thousands per month

- Staying put. Not upgrading when income increases. The mortgage on a home bought in 2015 looks very different from 2026 prices

Cheap Hobbies

This sounds trivial but it's not. Entertainment spending can quietly eat $500-$1,500/month. The $80K NorCal poster? A gamer. Total hobby cost: a gaming PC every few years and a modest internet bill. Other common normal-salary FIRE hobbies: hiking, cooking, reading, running, open-source projects.

Consistent Index Fund Investing

No stock picking. No crypto speculation. No complicated strategies. Every single normal-salary FIRE achiever in our data did the same thing: regular contributions to low-cost index funds, month after month, year after year. Dollar-cost averaging. No timing the market. Boring works.

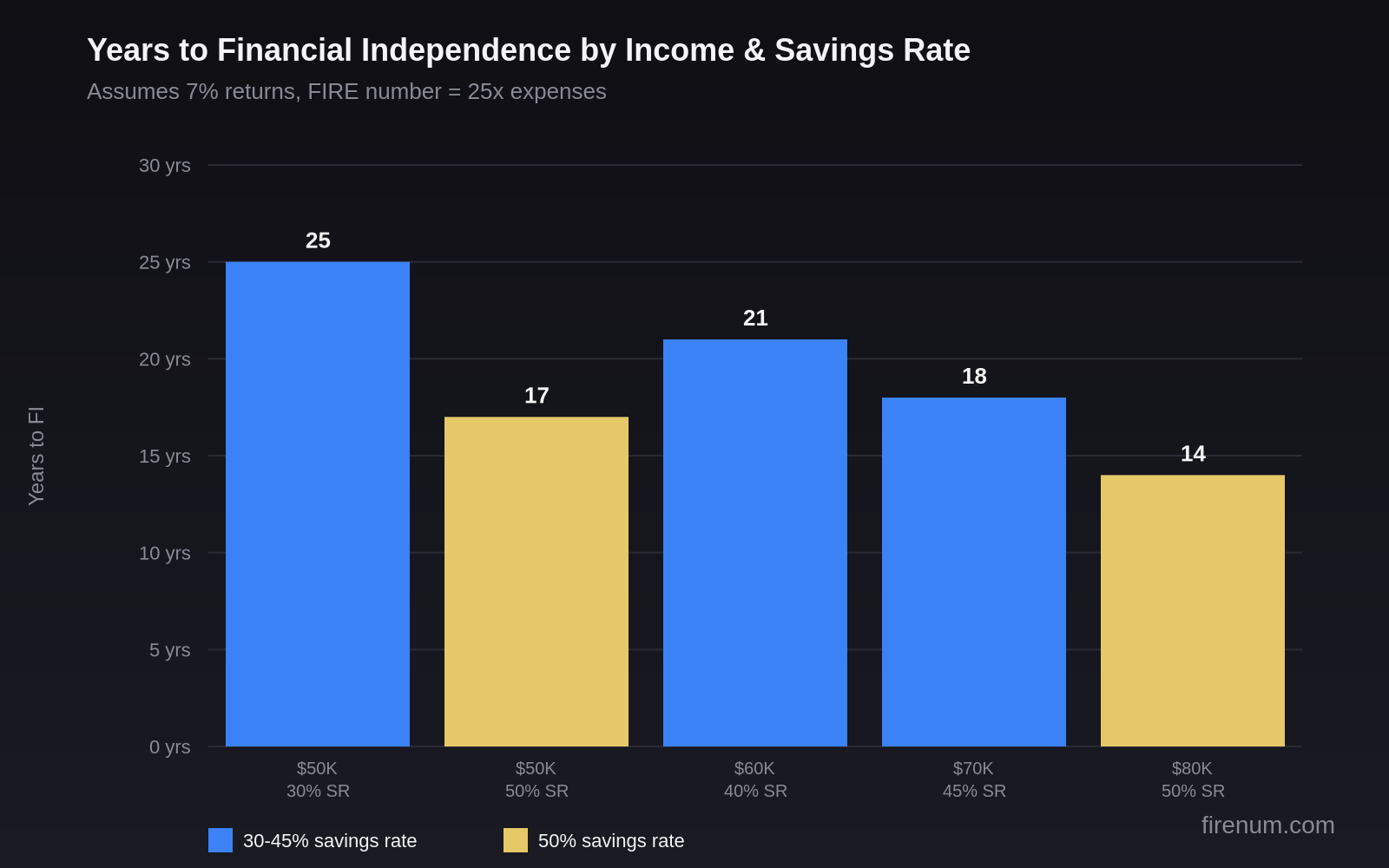

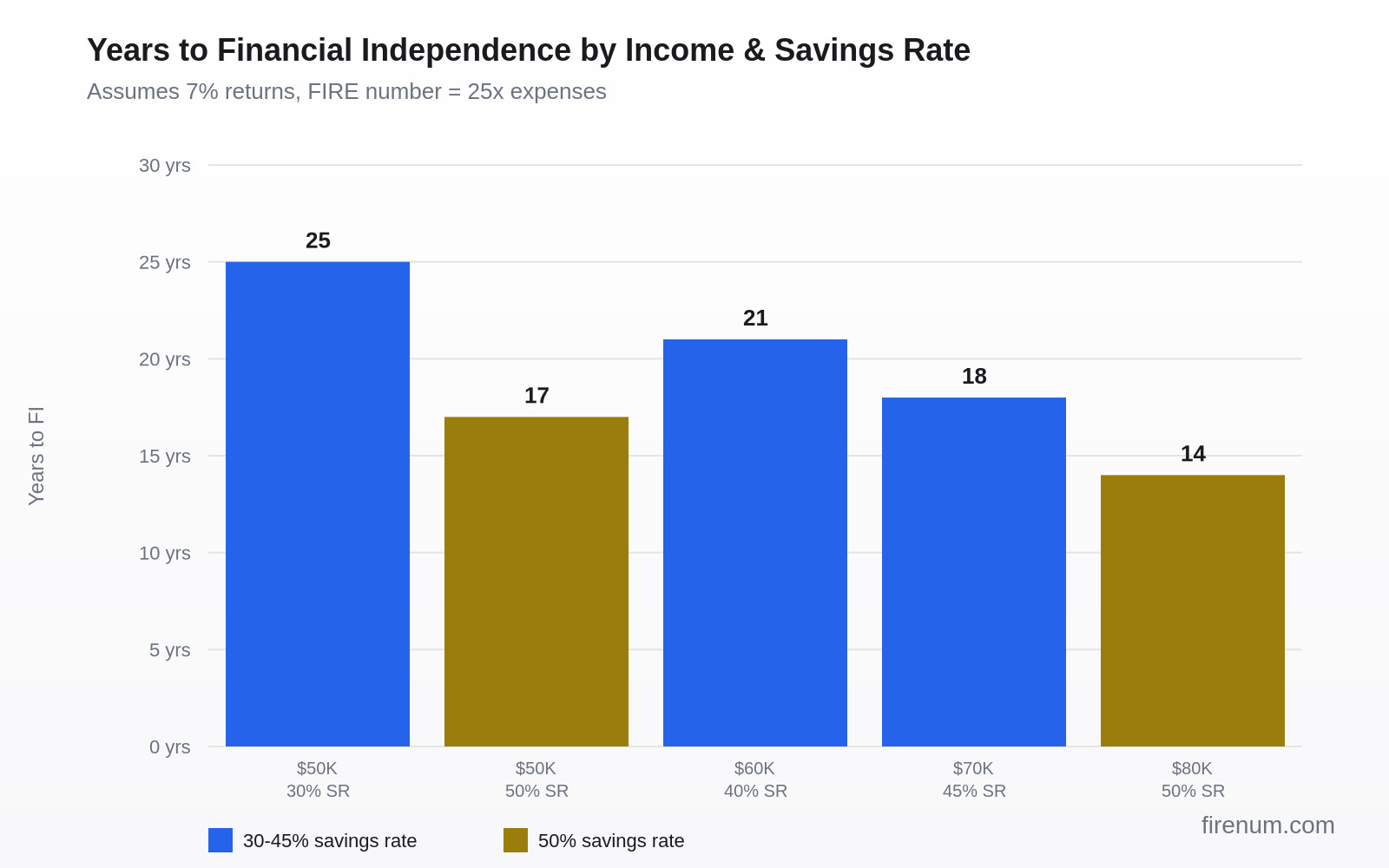

The Math at Different Income Levels

Here's how long it takes to reach financial independence at various income and savings rate combinations. Assumes 7% nominal returns, 3% inflation, and a FIRE number of 25x annual expenses.

| Annual Income | Savings Rate | Annual Savings | Annual Expenses | FIRE Number | Years to FI |

|---|---|---|---|---|---|

| $50,000 | 30% | $15,000 | $35,000 | $875,000 | ~25 years |

| $50,000 | 50% | $25,000 | $25,000 | $625,000 | ~17 years |

| $60,000 | 40% | $24,000 | $36,000 | $900,000 | ~21 years |

| $70,000 | 45% | $31,500 | $38,500 | $962,500 | ~18 years |

| $80,000 | 50% | $40,000 | $40,000 | $1,000,000 | ~14 years |

Notice the pattern: savings rate determines years to FI more than income does. Someone earning $50,000 at a 50% savings rate reaches FI in roughly the same time as someone earning $70,000 at 45%.

Run your own numbers. Use our When Can I Retire calculator to see your exact timeline.

What Nobody Tells You About Low-Income FIRE

Let's be honest about the challenges. This isn't just "save more and you'll be fine." There are real trade-offs.

It Takes Longer

A 25-year timeline starting at 25 means FIRE at 50. That's still early retirement by any definition, but it's not the "retire at 35" stories that get upvoted on Reddit. Patience isn't glamorous. It works anyway.

Emergency Fund Is More Critical

When your margin is thin, one unexpected $5,000 expense can derail months of progress. Normal-salary FIRE people need a larger emergency buffer relative to their income -- 6 months minimum, ideally closer to 12. This slows the early phase but prevents catastrophic setbacks.

Healthcare Is the Biggest Wildcard

In the US, employer-sponsored health insurance is effectively a $15,000-$25,000/year benefit. Losing that in early retirement changes the math dramatically. ACA subsidies help at lower income levels, but healthcare planning is non-negotiable for normal-salary FIRE.

The Bureau of Labor Statistics reports that median household income in the US is approximately $59,000. FIRE on a "normal salary" is FIRE at the actual median — not the Reddit-inflated version.

Lean FIRE Might Be the Realistic Target

If you're earning $50,000-$60,000, your FIRE lifestyle will likely be in the Lean FIRE range: under $40,000/year in expenses. That's perfectly livable in most of the US, especially with a paid-off home. But it requires being honest about what your retirement will look like.

Coast FIRE as an Intermediate Milestone

For many normal-salary earners, Coast FIRE is the game-changer. Save aggressively in your 20s and early 30s, then stop contributing and let compound growth carry you to a traditional retirement. You don't fully retire early, but you eliminate the pressure to save -- and that changes everything about how you experience work.

Real Stories From Normal-Salary FIRE Achievers

"Started investing at 22 making $45K as an admin assistant. Never made more than $72K. Hit $800K at 41 by living with roommates, driving used cars, and putting 45% of every paycheck into VTSAX. My friends thought I was cheap. I thought I was buying my freedom." -- 41M, admin/operations, $800K net worth

"Teacher for 18 years. Maxed my 403b every year once I hit year 3. Pension plus $650K in investments. I'm not technically FIRE'd but I hit Coast FIRE at 38 and now I teach because I want to, not because I have to. That shift in mentality is worth more than any dollar amount." -- 43F, teacher, $650K invested + pension

"Dual income but neither of us broke $60K. Combined we earned about $105K, saved 40% for 16 years. Hit $1.1M last month. No inheritance, no windfalls, no stock options. Just two boring index funds and a lot of saying 'no' to things we didn't really want anyway." -- 42M, married, combined $105K income

"I'm a nurse making $68K in a mid-size city. Hit $500K at 33 and I'm on track for $1M by 40. The biggest thing was buying a house at 25 and getting a roommate for the first 5 years. My housing cost was essentially $400/month. That single decision accelerated everything." -- 33F, nurse, $500K net worth

The common thread: none of these people had a magic income event. No startup IPO, no inheritance, no six-figure raise. They had time, consistency, and a savings rate that their peers considered unreasonable.

Getting Started

If you're earning $50,000-$80,000 and wondering whether FIRE is for you, here's the honest truth: it is, but you need to go in with eyes open.

- Calculate your number. FIRE Number Calculator -- takes 10 seconds

- Know your savings rate. If it's under 20%, that's the first thing to fix

- Automate your investing. Set up automatic monthly transfers to a total market index fund

- Attack housing costs. This is where the biggest wins live at normal incomes

- Set intermediate milestones. Coast FIRE, then Barista FIRE, then full FI

- Track your progress. Seeing the numbers grow keeps you motivated during the long middle

The path is longer on a normal salary. But "longer" still means decades earlier than the people who never start. And as every normal-salary FIRE achiever will tell you: the freedom starts before you reach the number. It starts the moment you know you have options.

Frequently Asked Questions

Yes. The math works at any income level. At $50K with a 50% savings rate, you're saving $25K/year. With 7% average returns, that reaches roughly $1M in about 17 years. You'd likely target Lean FIRE ($25K-$40K annual spending), which is achievable. It takes longer than high-income FIRE, but the math is the same.

It depends almost entirely on your savings rate, not your income. At a 30% savings rate, expect roughly 25 years. At 50%, roughly 17 years. At 60%, roughly 12-13 years. The higher your savings rate, the less your income matters because you're simultaneously saving more and proving you can live on less.

Both help, but spending less has a double effect: it increases your savings rate AND reduces the amount you need to retire. Cutting $500/month from expenses means $6,000 more saved per year and $150,000 less needed for your FIRE number ($6K x 25). That said, if you can increase income without increasing lifestyle, do both.

For someone spending $30K-$40K per year, the FIRE number is $750K-$1M (annual expenses x 25). Many normal-salary FIRE achievers target Lean FIRE in the $600K-$1M range. This is attainable on a $50K-$80K salary with discipline and time.

No, but it's the most common path. Coast FIRE is another great intermediate target -- save aggressively in your 20s and 30s, then stop contributing and let compound growth do the rest. Some normal-salary earners also reach traditional FIRE by combining strategies: geographic arbitrage, housing hacks, side income, and long time horizons.

First, build a small emergency fund ($1K-$2K). Then attack high-interest debt (credit cards, personal loans) aggressively. For lower-interest debt like student loans, you can invest simultaneously if returns exceed the interest rate. Many FIRE achievers carried mortgage debt throughout their journey. The key is eliminating consumer debt first, then redirecting those payments to investments.

Ready to run the numbers?